Table of contents (55)

- What It Takes

- The gap nobody warns you about

- What "operationally ready" actually requires

- The cleaner path for most first hires

- Shipping Nightmare

- The "running with scissors" move

- What actually happens at the border

- Why the ticket queue makes it worse

- Choosing a Model

- Three doors, one decision

- The decision matrix

- How to read it

- Where each model breaks

- Our default, and why

- Tax-Smart Stipends

- Lead with the rule, because money is at stake

- Why this hits your costs

- The compliant way to structure equipment

- Layering tax-smart take-home

- DPDP Device Compliance

- Why a laptop is now a compliance surface

- The three things the rules actually ask

- What this means for the device itself

- MDM Is Mandatory

- The device you will never touch

- Enroll before you ship, not after

- Why this beats monitoring software

- Asset Recovery

- The day a resignation lands in Coimbatore

- Why generic recovery fails

- The lever that actually works

- What I have learned doing this

- True Cost Per Hire

- The number that surprises CFOs

- The full cost stack

- The PF ceiling shift you must model

- Where the cost actually drops

- PE and Multi-State Risk

- The talent shows up in a Tier-2 city

- Three risks that bite quietly

- How an owned entity absorbs it

- Your Monday check

- Owned Entity and SLA

- The hidden middle layer

- What owned-entity ownership unlocks

- The 5-day SLA, day by day

- Where this still breaks

- Versatile vs Competitors

- Too many tabs, no clear answer

- The comparison matrix

- Who should not pick us

- Cost or Trust Pipeline

- The line item that lies

- Build a jazz band, not an orchestra

- Where my head is right now

Equip Remote Employees in India: Provisioning, Stipends, MDM & Asset Recovery Guide | June 2026

Equip remote employees in India in 2026 without an entity. Discover compliant provisioning, MDM security, and true cost per hire for global teams.

Q1: What does it actually take to equip a remote employee in India in 2026?

Equipping a remote employee in India means three things landing together: a compliant employment setup, a configured device in their hands by Day 1, and security plus tax structuring that survives an audit. You do not need your own Indian entity to do this. An India-native EOR that owns its entity can procure, configure, and own the asset on your behalf, which avoids cross-border customs friction.

The gap nobody warns you about

Last year a US founder messaged me at 11 PM his time. His new Bengaluru engineer had signed, badged in, and had no laptop. The contract was perfect. The hire was not working.

That is the gap I see most often. People treat "compliant hire" and "ready hire" as the same thing. They are not. A signed agreement does not write code.

What the reader actually wants

After six years placing engineers, designers, and ops staff across Bengaluru, Hyderabad, and Pune, I have learned to flip the question. The reader does not want a legal hire. They want someone productive by Friday.

What "operationally ready" actually requires

Think of it as three layers stacked on the same day. Miss one, and the hire stalls.

- ✅ Employment layer: A compliant contract, plus PF (Provident Fund, a retirement deduction), ESI (state health insurance), and TDS (tax deducted at source) running from Day 1.

- ✅ Device layer: A configured laptop, accessories, and software in the employee's hands, ideally before the start date.

- ✅ Security and tax layer: Device security enrolled, and any stipend structured so it does not trigger a tax or payroll problem later.

The entity myth

A common myth says you must register your own Indian company to give someone a laptop. You do not.

The cleaner path for most first hires

You can hire and equip through an Employer of Record. The EOR is the legal employer in India and, if it owns its entity, the legal owner of the device too.

We do this through our own registered Indian entity. That means the laptop is bought locally on our GSTIN (the GST tax ID), owned by us, and handed to your employee. No customs. No 20% duty drama.

So the real answer to "what does it take" is not a checklist of forms. It is one partner who lands all three layers on the same Monday morning.

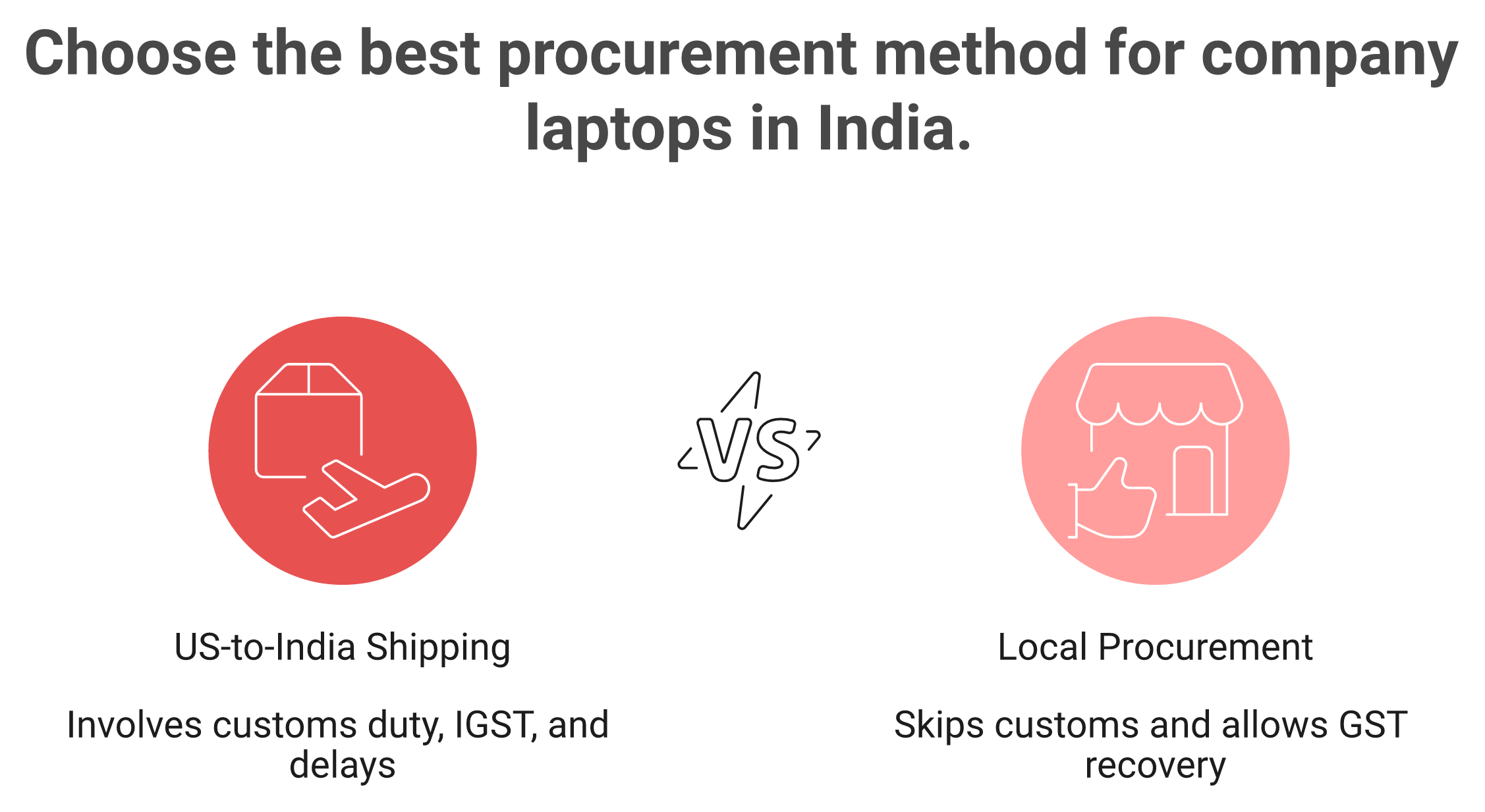

Q2: Why is shipping a laptop from the US to India a compliance nightmare?

Shipping a company laptop from the US to India attracts roughly 20% customs duty plus 18% GST on declared value, can raise BIS considerations, and routinely stalls in customs for days. For a single device, the landed cost and delay rarely justify the model. That is why 2026 best practice favours buying locally through an Indian entity's GSTIN.

The "running with scissors" move

I call US-to-India shipping the "running with scissors" move. It feels fast. It usually ends in blood.

A founder pictures a clean courier path. Pack the MacBook, ship it, done. India's customs system does not work that way.

What actually happens at the border

Here is the friction stack, layer by layer.

- 💰 Customs duty: A new imported laptop attracts duty around 20% of declared value.

- 💰 GST on import: Add roughly 18% IGST on top of the duty-inclusive value.

- ⚠️ BIS rules: Electronics can trigger Bureau of Indian Standards registration questions, which slow clearance.

- ⏰ Customs hold: A single high-value device can sit in customs for days while paperwork clears.

The real cost of a $1,500 laptop

So a $1,500 laptop is not a $1,500 problem. After duty, IGST, courier fees, and insurance, the landed cost climbs sharply. And the employee still has nothing.

Why the ticket queue makes it worse

The real pain is not the math. It is the silence when the device is stuck.

I have had a device flagged at clearance on a Friday. We solved it on WhatsApp before the weekend, with the actual person who runs the entity. A global generalist often routes you to a ticket queue and a three-day SLA.

The fix, in one line

Stop shipping. Buy locally through an Indian entity's GSTIN.

Local procurement skips customs entirely, recovers GST as input credit, and lands the device in days, not weeks. The next section shows when shipping still makes sense, and when it never does.

Q3: IOR shipping vs. local procurement vs. stipend: which model should you choose?

Choose local procurement through your Indian entity's GSTIN as the 2026 default. It is fastest, GST-recoverable, and avoids customs friction. Use IOR (Importer of Record) shipping only for a specific corporate-imaged device unavailable locally. Use a stipend when speed and simplicity beat control, accepting that stipends are taxable salary unless reimbursed against bills.

Three doors, one decision

Every founder I talk to faces the same three doors. Most pick the wrong one because nobody scored them side by side.

So here is the honest scorecard, based on what surfaces when you actually run this.

The decision matrix

| Model | Speed | Cost / tax | Compliance risk | Control | Best for |

|---|---|---|---|---|---|

| Local procurement (GSTIN) ✅ | Fast (days) | GST recoverable as input credit | Low | High (entity owns asset) | Most India hires in 2026 |

| IOR shipping | Slow (weeks) | ~20% duty + 18% GST | Medium (BIS, customs) | High (your exact image) | A specific corporate-imaged device only |

| Stipend / reimbursement | Fastest | Taxable salary unless billed | Medium (perquisite risk) | Low | Speed over control, short engagements |

How to read it

Local procurement wins on the two things founders feel most: time and cash. The device lands in days, and the GST comes back as input credit, so the real cost drops.

IOR shipping is not useless. It is just narrow. Use it only when you need an exact corporate-imaged machine that you cannot buy in India.

When a stipend is the right call

A stipend looks easy, and sometimes it is the right call. But money handed over as allowance is taxable salary unless it is a proper reimbursement against bills.

Where each model breaks

- ❌ Local procurement not recommended for: teams that need one identical hardware image across 40 countries on Day 1.

- ❌ IOR shipping not recommended for: a single laptop to a single new hire. The duty and delay rarely pay off.

- ❌ Stipend not recommended for: roles handling sensitive IP, where you need MDM control before the device is live.

Our default, and why

We coordinate local procurement inside onboarding, on our own GSTIN. The entity owns the asset, so recovery later is clean.

I might be wrong for a 50-country rollout. For a first India hire, the standard "just ship it" read gets this backwards.

Q4: How do you structure tax-smart equipment stipends under the New Labour Codes?

Since the Labour Codes took effect on 21 November 2025, wages (basic plus DA) must be at least 50% of total CTC, and excess allowances get added back to wages, raising PF and gratuity. Keep equipment as company-owned assets or reimbursement, not loose allowance. Layer tax-smart tools, meal and fuel cards and NPS under Section 80CCD, to lift take-home without tripping the wage line.

Lead with the rule, because money is at stake

Here is the headline first. A fat "equipment allowance" parked in the allowance bucket can quietly raise your statutory bill.

The Code on Wages now sets a uniform definition. Basic plus DA (dearness allowance) must be at least half of CTC. Anything you stuff into allowances beyond that gets added back to wages.

Why this hits your costs

PF is calculated on wages. Gratuity accrues at 4.81% of basic plus DA. Push more into "wages," and both rise.

So a stipend you meant as a perk can inflate PF and gratuity for every affected hire. That is the misclassification trap, and it surfaces in due diligence at the worst time.

The compliant way to structure equipment

After running multi-state PF, ESI, and PT compliance through real placements, here is what I would do on Monday.

- ✅ Company-owned asset: Buy the laptop on the entity and own it. A company device used for work is generally not a taxable perquisite for the employee.

- ✅ Reimbursement against bills: If the employee buys, reimburse against actual invoices, not a flat cash allowance.

- ❌ Avoid: A loose monthly "equipment allowance," which reads as taxable salary and can breach the 50% line.

Layering tax-smart take-home

Beyond hardware, you can lift net pay without raising tax.

- 💰 Meal and fuel cards: Structured benefit instruments that increase take-home within defined limits.

- 💰 NPS under Section 80CCD: Employer contribution to the National Pension System is a recognised deduction that helps high earners.

Where transparency beats surprises

We file PF, ESI, TDS, and professional tax under our own registrations across states, through our India payroll operations. That is the difference between transparency and a surprise.

The payoff is simple. Structure equipment as an asset or reimbursement, keep allowances under the 50% line, and your hire keeps more without you carrying audit risk.

Q5: What does DPDP Act compliance demand from devices given to Indian employees?

The DPDP Rules 2025, notified on 13 November 2025, require lawful handling of personal data on company devices, defined retention, and breach reporting to the Data Protection Board within 72 hours, with most obligations enforceable by 14 May 2027. In practice, this means encrypted, MDM-enrolled devices with clear retention and wipe policies, framed against Indian law, not GDPR.

Why a laptop is now a compliance surface

A device handed to your India hire is not just hardware. It holds personal data, and that makes it a legal surface under the DPDP Act.

The Digital Personal Data Protection Rules, 2025, were notified on 13 November 2025. Most operational duties become enforceable by 14 May 2027, so you have a real runway, not an excuse.

The three things the rules actually ask

Think of DPDP like a building code for data. It does not tell you the furniture. It tells you the safety rules.

- ✅ Lawful handling: Personal data on the device must be collected and used for a clear purpose.

- ⏰ Defined retention: You keep data only as long as needed, then delete it.

- ⚠️ 72-hour breach reporting: A reportable breach must reach the Data Protection Board within 72 hours.

Why GDPR habits mislead here

I see US founders reach for GDPR habits here. That is the wrong map. India has its own law now, and it does not mirror Europe one-to-one. Strong India-specific compliance handling closes that gap.

What this means for the device itself

This is where data law meets the laptop on someone's desk in Pune.

- 🔒 Encryption: Full-disk encryption, so a lost device does not leak data.

- 🔒 MDM control: Mobile Device Management to push policy and wipe remotely (more on this next).

- 🔒 Retention and wipe policy: A written rule for what gets deleted, and when.

How we build it in

We bake device data policy into our EOR provisioning, not as an afterthought. The asset ships secured, because retrofitting security after a breach is the expensive way to learn this.

I could be off on the exact enforcement pace. Where my head is right now: build for the 2027 deadline today, because audits look backward.

Q6: Why is MDM no longer optional for remote engineers in India?

Mobile Device Management (MDM) is the baseline now, not a nice-to-have, because remote engineers handle source code and customer data on devices you cannot physically see. Enroll devices in MDM (Microsoft Intune, Windows Autopilot, or equivalent) before they reach the employee, so encryption, VPN, and remote-wipe are active on Day 1. This protects IP and satisfies DPDP obligations at the same time.

The device you will never touch

Your engineer in Hyderabad has your source code on a laptop you will never hold. That is the quiet risk nobody puts on the onboarding checklist.

MDM is how you manage a device you cannot see. It enforces encryption, pushes a VPN, and lets you wipe a lost machine remotely.

Enroll before you ship, not after

The mistake I see most is enrolling devices after the employee logs in. By then, the unprotected window is already open.

Here is the order that works.

- ✅ Procure and image: Buy the device and load the corporate image.

- ✅ Enroll in MDM: Register it in Intune or Autopilot before dispatch.

- ✅ Push policy: Encryption, VPN, and access rules go live.

- ✅ Hand over secured: The employee receives a device that is already locked down.

How our onboarding handles it

We enroll and image devices before dispatch as standard, inside a structured India team build. The engineer's first login happens on a managed machine, so Day 1 is also Day 1 of security.

Why this beats monitoring software

Some founders confuse MDM with surveillance. They are different things, and the difference matters for trust.

MDM secures the device. Monitoring software watches the person. I lean hard toward the first and away from the second.

"Support is the single biggest failure. There is no direct phone line. You either email or use a chatbot, and you can ask both the same question and get two different wrong answers."

Erika D., Verified User Rippling G2 Verified Review

That review is about a different problem, but it points at the same nerve. When a managed device misbehaves, a chatbot cannot fix it. A person can.

"Often the CS doesn't seem to have answers, which leads me to emails back and forth on my case, and something I was looking for the answer to in 20 minutes becomes a 4-day process."

Verified User in Computer Software Deel G2 Verified Review

When a device is locked and an engineer cannot work, a four-day ticket loop is a four-day outage. That is why I keep founder-led support on WhatsApp, not in a queue.

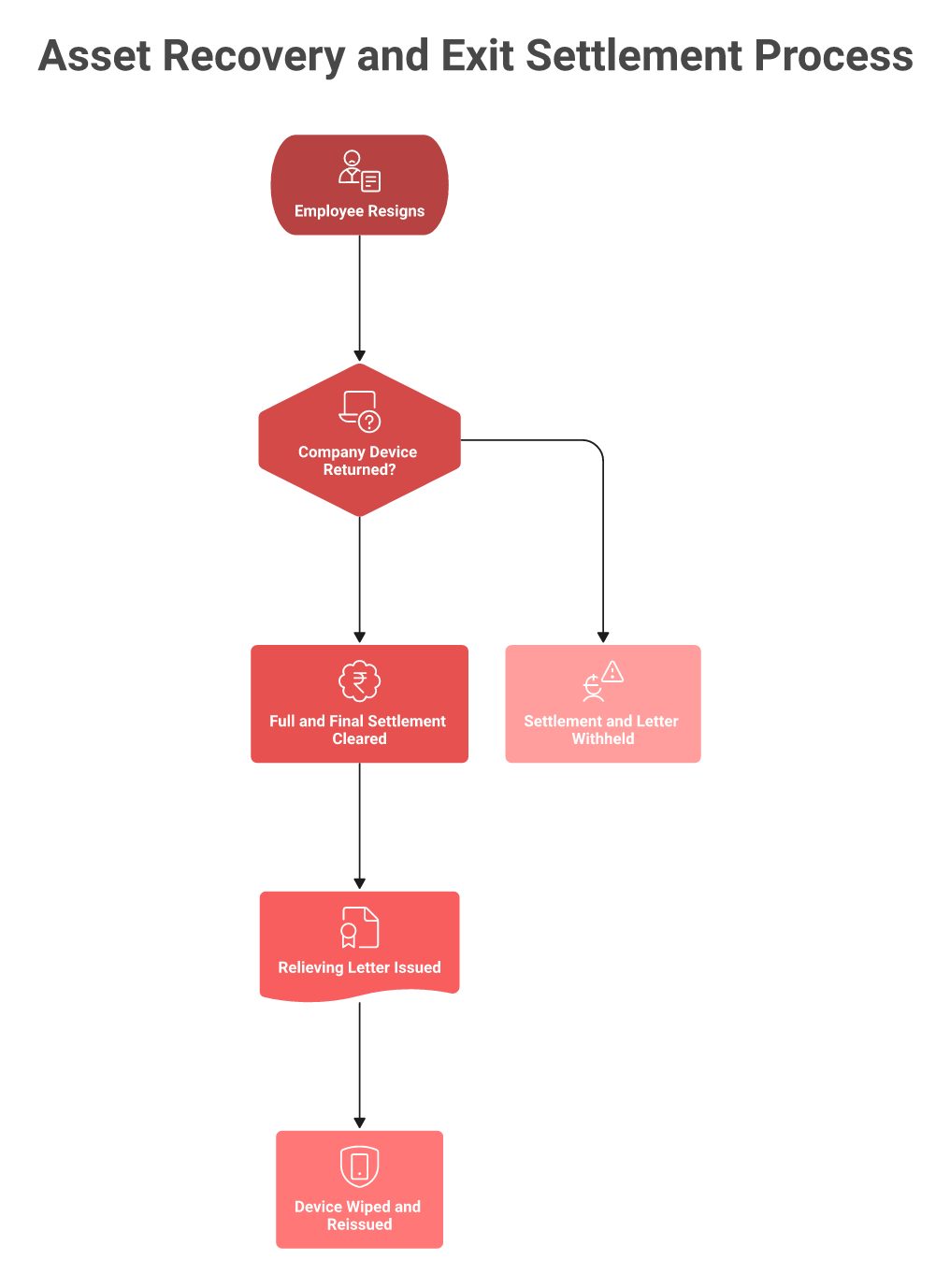

Q7: How do you recover a laptop when an employee in a Tier-2 city quits?

Tie hardware recovery to the employee's Full and Final (F&F) settlement and the Relieving Letter. Company property must be returned, or its value adjusted, before the final settlement clears and the relieving letter issues. With an owned Indian entity as the legal asset owner, this is enforceable and clean, versus a partner-shell model where ownership is murky.

The day a resignation lands in Coimbatore

Picture this. Your engineer in Coimbatore resigns on a Tuesday. The laptop, with your source code, is in their home, eight hundred kilometres from anyone you know.

This is the scenario competitors gloss over. Asset recovery is the shallowest section in most equipping guides, and it is the one that keeps founders up at night.

Why generic recovery fails

The complication is ownership. If your EOR uses a local-partner shell, who legally owns that laptop?

That gap turns a simple return into a slow, awkward negotiation. Nobody is sure who can compel the device back.

The lever that actually works

In India, the strongest, cleanest lever is the exit settlement itself. You connect the device to money the employee is owed.

- ✅ Link to F&F: The Full and Final settlement, the last payout, clears only after company property is returned or its value is adjusted.

- ✅ Gate the Relieving Letter: This document, which the employee needs for their next job, issues after asset return.

- ✅ Secure wipe: Once recovered, the device is wiped under your retention policy before reuse.

Why owning the entity matters

We own the Indian entity, so we are the direct legal owner of the asset, managed through our India EOR services. Recovery is a clear instruction from the owner, not a plea through a middle layer.

What I have learned doing this

Across placements we have offboarded, the pattern is simple. Recovery that is tied to F&F almost always works. Recovery that relies on goodwill alone often does not.

I might be wrong for senior, long-tenure exits where trust carries it. For most exits, the standard "just ask nicely" read gets this backwards. The payoff is control. The asset comes back, the data is wiped, and the relieving letter goes out clean.

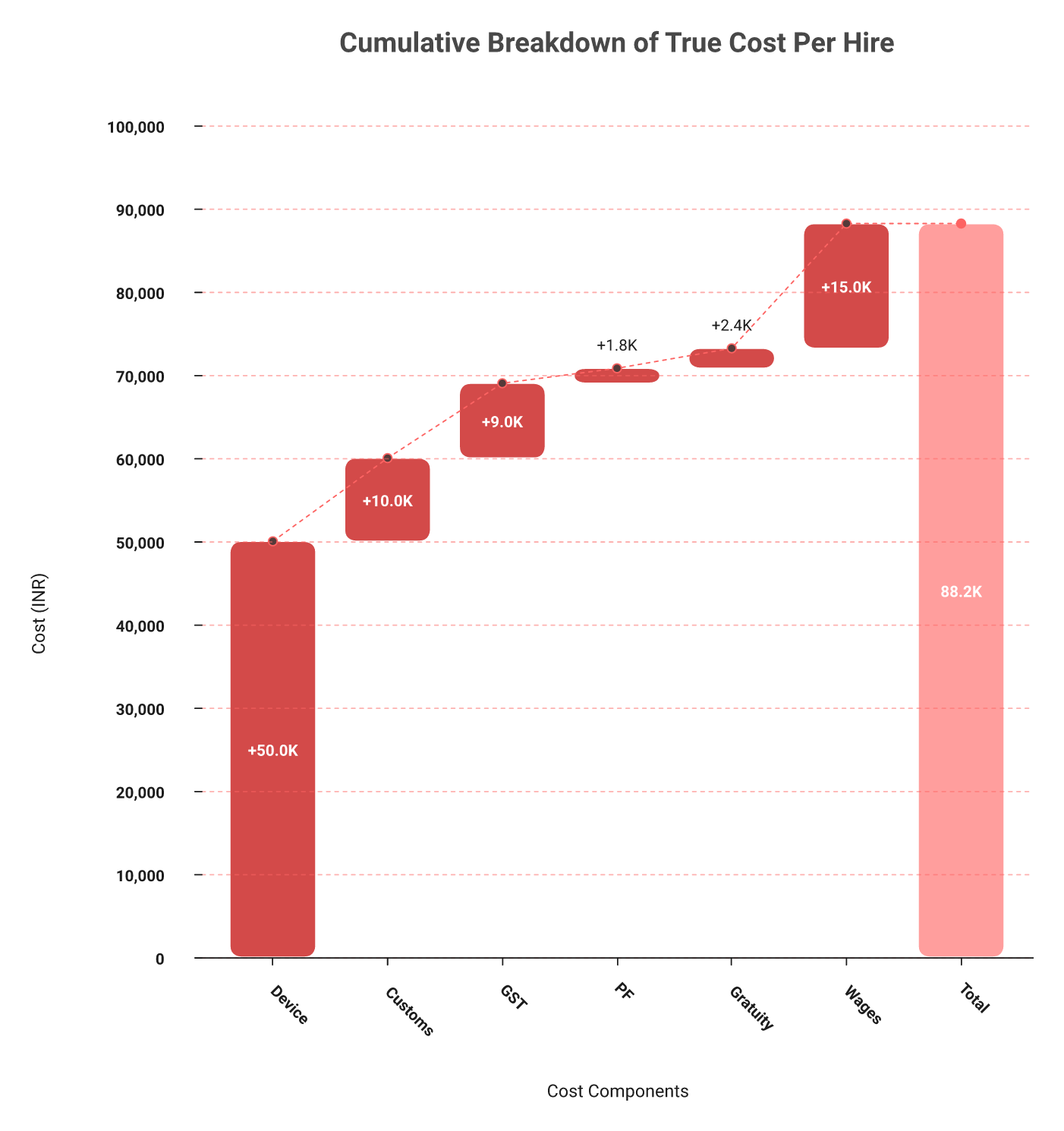

Q8: What is the true total-cost-per-hire, and where do leasing and GST refunds cut it?

True cost-per-hire is more than the laptop. Add device cost, any customs duty (~20%) and GST (18%) if shipped, employer PF (capped today at the ₹15,000 wage ceiling, with a hike toward ₹25,000 under consideration), gratuity under the 50% wage rule, and state-specific minimum wages. Leasing and GST input-credit recovery can cut device spend meaningfully.

The number that surprises CFOs

Founders budget for the laptop price. They forget the laptop drags a tail of duty, tax, and statutory cost behind it.

In our work with CFOs at $5M to $50M ARR SMBs, this is the line that surprises them at month-end. The device is the small part.

The full cost stack

| Cost component | What it is | Rough scale |

|---|---|---|

| 💻 Device | Laptop plus accessories | One-time |

| 💰 Customs duty (if shipped) | Import duty on the device | ~20% of value |

| 💰 GST / IGST (if shipped) | Tax on import | ~18% |

| 💰 Employer PF | Provident Fund, 12% of wages | Capped at ₹15,000 ceiling today |

| 💰 Gratuity accrual | 4.81% of Basic plus DA | Ongoing |

| 💰 State minimum wage | Varies by state and skill | State-specific |

The PF ceiling shift you must model

PF today is capped at the ₹15,000 monthly wage ceiling. But that ceiling is under active review, with a transition toward ₹25,000 being considered.

So model both. A jump to ₹25,000 raises employer PF cost per hire, and an honest forecast prices in the change before it lands. Our cost-of-hiring breakdown models exactly these layers.

Where the cost actually drops

You are not stuck with the gross number. Two levers cut it.

- ✅ GST input credit: Buy locally on the entity's GSTIN, and recover the GST as input credit instead of eating it.

- ✅ Leasing: Lease devices instead of buying, which spreads the spend and eases the cash hit.

One clean number for finance

We invoice in USD from a single Indian entity, through transparent India payroll operations, with no FX exposure and no setup or exit fees. The CFO sees one clean number, not a currency puzzle.

The payoff is a cost-per-hire you can defend in a board deck, not one that surfaces as a surprise in diligence.

Q9: Where do PE risk, FEMA/FC-GPR, and multi-state rules bite distributed teams?

A distributed India team creates risks device-focused guides ignore: Permanent Establishment (PE) exposure from a fixed place or dependent agent, FEMA/FC-GPR obligations on inbound equity, and 28 distinct state Shops and Establishments plus professional-tax regimes. Hiring across Jaipur, Coimbatore, and Pune means each state's minimum wage and registration applies. An EOR that owns the entity absorbs this.

The talent shows up in a Tier-2 city

A founder finds a brilliant engineer in Jaipur. Then another in Coimbatore. Suddenly, the team is spread across three states, and so is the risk.

This is the layer most equipping guides skip entirely. They treat India as one place. India is not one place for compliance, which is why India-native EOR services matter.

Three risks that bite quietly

Here is my governing claim. A distributed team multiplies exposure on three fronts at once.

- ⚠️ PE risk: A "Permanent Establishment" is a taxable presence. A fixed place or a dependent agent acting for you can create one, pulling your foreign company into Indian tax. You can gauge this with a PE risk quiz.

- ⚠️ FEMA / FC-GPR: If you fund an Indian entity with equity, FEMA rules require an FC-GPR filing for that inbound investment.

- ⚠️ Multi-state rules: Each state runs its own Shops and Establishments Act, professional tax, and minimum wage.

Why the state detail matters

The state detail is where generic players stumble. Maharashtra needs PTRC and PTEC. Karnataka runs monthly professional tax. Tamil Nadu files professional tax twice a year. Delhi has no PT but strict S&E rules.

How an owned entity absorbs it

This is "India-native, not bolted-on." We hold PF, ESIC, and Shops and Establishments registrations across all 28 states and 8 union territories, the backbone of our India payroll operations.

So, when your hire signs in Coimbatore, the right state registration already exists. You do not assemble it under deadline pressure. We carry the multi-state machinery, so you do not inherit the exposure.

Your Monday check

Before your next Tier-2 hire, ask three questions. Could this create PE exposure? Is the funding FEMA-compliant? Is the state's PT and S&E covered? An India cost-of-hiring breakdown helps you price the answer.

I could be off on edge cases for unusual structures. For a standard distributed team, the standard "India is one country" read gets this backwards.

Q10: Why does owning the Indian entity and a 5-day SLA beat a partner shell?

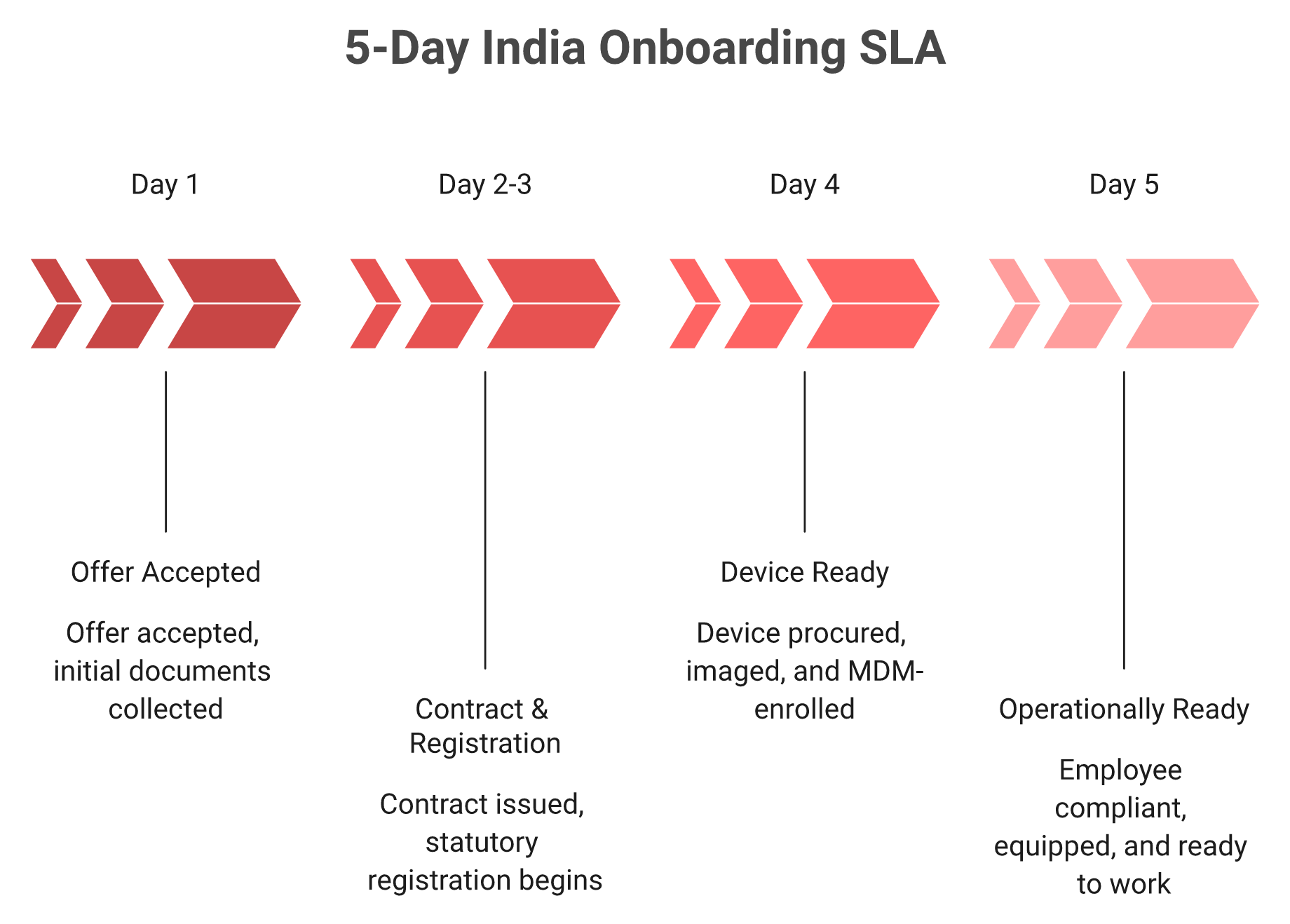

When the EOR owns the Indian entity, it is the direct legal owner of the laptops and direct filer of PF, ESI, TDS, and professional tax, so recovery and audits are clean. That ownership also enables a contractual 5-day onboarding SLA, where statutory registration and hardware readiness run in parallel and complete around Day 4, versus partner-shell models that add a slow middle layer.

The hidden middle layer

Many global EORs do not own an Indian entity. They route you through a local partner. That adds a layer between you and the company that holds your assets and files your taxes.

I think of it like cloud regions. A provider with its own regional infrastructure moves faster than one renting space from a local host. Ownership is depth, which is the core of the EOR versus entity decision.

What owned-entity ownership unlocks

The benefits are concrete, not abstract.

- ✅ Direct asset ownership: We own the laptop, so recovery is a clear instruction, not a negotiation through a partner.

- ✅ Direct statutory filing: PF, ESI, TDS, and professional tax run under our own registrations.

- ✅ Clean audits: One owner, one paper trail, no finger-pointing between layers.

The 5-day SLA, day by day

Ownership is what makes speed contractual. Here is how the parallel onboarding runs through our India EOR.

- ⏰ Day 1: Offer accepted, documents collected.

- ⏰ Day 2 to 3: Contract issued, statutory registration begins.

- ⏰ Day 4: Device procured locally, imaged, and MDM-enrolled.

- ⏰ Day 5: Employee is operationally ready, compliant, and equipped.

How this compares

We run this on a 5-day contractual SLA, the speed that powers a fast India team build. A global generalist often quotes one to two weeks, partly because the partner-shell handoff slows everything.

Where this still breaks

I will name the honest limit. If your procurement team demands a fully customized enterprise workflow, that takes longer than five days. The SLA fits the first-hire and scaling-team case, not a 100-person enterprise rollout with bespoke security review.

The payoff for most of you is simple. The hire is ready by Friday, not next month.

Q11: Versatile vs. Wisemonk vs. global generalists: how do you decide?

Pick Versatile when you want an India-native partner that owns its entity, invoices in USD directly from India, commits to a 5-day onboarding SLA, gives you the founder on WhatsApp, and backs hires with a 6-month replacement guarantee and no setup or exit fees. Pick a global generalist only if you genuinely need 100-plus countries on one contract.

Too many tabs, no clear answer

You have ten browser tabs open. Wisemonk, Deel, Remote, Multiplier. They all promise India. The pricing pages blur together.

So, here is the honest scorecard, with Versatile first because India is all we do. You can also weigh the Wisemonk versus Versatile comparison directly.

The comparison matrix

| Criterion | Versatile ✅ | Wisemonk | Global generalists (Deel, Remote, G-P) |

|---|---|---|---|

| India model | Owned Indian entity | India-native | Often local-partner shells |

| Onboarding | 5-day contractual SLA | 24 to 72 hrs | 7 to 14 days |

| Support | Founder on WhatsApp | Team support | Ticket queue / chatbot |

| Retention | 90-day Success Coach, 6-month replacement guarantee | No published guarantee | Not India-specific |

| Fees | No setup or exit fees, first month free | $99 anchor | $400 to $599 / employee |

To be fair, Wisemonk is a real India-native operator with SOC 2 and ISO 27001 and a strong G2 record. Buyers like its structure, though many still weigh Wisemonk alternatives.

"What I like most about WiseMonk is how they convert a complex international hiring process into a structured and easy workflow."

Verified User in Marketing and Advertising Wisemonk G2 Verified Review

The honest gaps show up in support depth and the retention story.

"I've noticed that their support query responses can occasionally take a bit longer sometimes, likely due to a relatively small team."

Verified User in Financial Services Wisemonk G2 Verified Review

Global generalists carry their own well-documented India pain.

"It took three months to onboard our first 3 individuals. They didn't seem to be able to navigate Visas or variations to employment contracts."

Verified User in Information Technology and Services Deel G2 Verified Review

Who should not pick us

I will say it plainly. If you need EOR in 15 countries, a generalist fits better. If you are a 100-plus India enterprise that makes SOC 2 a procurement gate, that is our Anti-ICP, and I will tell you so on the first call. For the right fit, see our best India EOR for startups breakdown.

Q12: Is equipping remote staff a cost or a trust pipeline?

Equipping remote staff well is not a cost line. It is a trust pipeline. High-quality hardware tells an India-based hire they are an equal part of the global team, not a bolted-on contractor. The founders who win in India provide the best tools and judge on output, rather than installing monitoring software that does more harm than good.

The line item that lies

Most founders file the laptop under "cost." I think that label hides what is really happening.

The first device you hand a new hire is a message. A fast, well-chosen machine says "you matter as much as the team in San Francisco." That signal sits at the heart of a retention-first EOR approach.

Build a jazz band, not an orchestra

Here is the part the category avoids saying. Surveillance software signals distrust, and distrust leaks into output.

I would rather build a jazz band than conduct an orchestra. Give the musicians great instruments and the key, then let them play. Judge the music, not the practice hours. That mindset shapes how we build India teams.

Compliance is the floor

Compliance is the floor here, never the ceiling. Across placements we have converted to full-time over six years, the hires who felt equipped from Day 1 stayed longer and shipped more.

Where my head is right now

What I think shifts in the next two years is this. India stops being one country on a global map and becomes its own specialist category, where owned-entity operators win the depth game. If you are weighing the build, our EOR versus entity guide is a good place to start.

So, I will leave you with a question, not a pitch. If your next India hire opened their laptop on Day 1, would it feel like an invitation, or an afterthought? If you are figuring that out, message me on WhatsApp and tell me what you are building.

FAQs

Can we equip a remote employee in India without setting up our own Indian entity?

Yes, you can fully equip an India hire without owning a local entity, and for most first hires we think that is the smarter route.

Equipping someone properly means three things landing on the same day:

- A compliant employment setup with PF, ESI, and TDS running from Day 1.

- A configured laptop in their hands, ideally before they start.

- Device security and tax structuring that survives an audit.

An Employer of Record that owns its Indian entity becomes the legal employer and the legal owner of the device. That ownership matters. It means the laptop is bought locally on the entity GSTIN, so you avoid roughly 20 percent customs duty plus 18 percent GST and the delays of cross-border shipping.

Setting up your own subsidiary can cost tens of thousands of dollars and take twelve to eighteen months before your first hire. We remove that barrier through our India EOR services, procuring, configuring, and owning the asset for you. If you want to weigh both paths honestly, our EOR versus entity comparison lays out the cost and timeline trade-offs in detail.

Why is shipping a laptop from the US to India such a compliance problem?

Shipping a company laptop into India looks simple and rarely is. A single new device attracts roughly 20 percent customs duty plus about 18 percent GST on declared value, and it can stall in customs for days.

The friction stacks up fast:

- Customs duty around 20 percent of declared value.

- IGST of roughly 18 percent on the duty-inclusive value.

- Bureau of Indian Standards registration questions on electronics.

- Multi-day customs holds while paperwork clears.

So a 1,500 dollar laptop is never a 1,500 dollar problem once duty, tax, courier fees, and insurance land. Meanwhile, your new engineer has nothing to work on.

The cleaner path in 2026 is buying locally on an Indian entity GSTIN, which skips customs entirely and recovers GST as input credit. We coordinate this inside onboarding, and you can see how we handle the alternative on our ship laptops to India page. For the wider tax mechanics behind local buying, our India GST and IT compliance resource explains the input-credit logic.

What does DPDP Act and MDM compliance require for devices given to India engineers?

The Digital Personal Data Protection Rules, 2025, notified on 13 November 2025, treat any device holding personal data as a compliance surface, with most obligations enforceable by 14 May 2027.

In practice, the rules ask for three things:

- Lawful, purpose-bound handling of personal data on the device.

- Defined retention, so data is deleted when no longer needed.

- Breach reporting to the Data Protection Board within 72 hours.

That is why Mobile Device Management, or MDM, is no longer optional. Tools like Microsoft Intune or Windows Autopilot let you enforce encryption, push a VPN, and remotely wipe a lost machine. We enroll and image devices before dispatch, so an engineer in Hyderabad or Pune logs in to a managed, secured machine on Day 1.

One caution: do not copy GDPR habits wholesale, because India has its own framework now. We build device data policy directly into provisioning, never as an afterthought. You can see how this fits a compliant build on our build a team in India page, supported by our broader India EOR services.

What is the true total cost per hire to equip an employee in India?

The laptop price is the small part. The true cost per hire carries a tail of duty, tax, and statutory components that surprises finance teams at month-end.

The full stack includes:

- Device cost, plus accessories.

- Customs duty (around 20 percent) and GST (about 18 percent) if shipped.

- Employer PF, currently capped at the 15,000 rupee wage ceiling, with a transition toward 25,000 rupees under consideration.

- Gratuity accrual at 4.81 percent of basic plus DA.

- State-specific minimum wages.

Two levers cut the number meaningfully. Buying locally on a GSTIN recovers GST as input credit, and leasing devices spreads the cash hit instead of a large upfront spend.

We invoice in USD from a single Indian entity, with no FX surprises and no setup or exit fees, so your CFO sees one clean, defensible number. To model your own scenario before committing, use our cost of hiring in India resource, and for a quick estimate, our employee cost calculator breaks down the statutory layers line by line.

How do we recover a company laptop when an India employee in a Tier-2 city resigns?

Asset recovery is the section most equipping guides gloss over, and it is the one that keeps founders up at night when a laptop with source code sits in a home eight hundred kilometres away.

In India, the cleanest lever is the exit settlement itself. You tie the hardware to money the employee is owed:

- Full and Final settlement, the last payout, clears only after company property is returned or its value is adjusted.

- The Relieving Letter, which the employee needs for their next job, issues after the asset returns.

- Once recovered, the device is wiped under your retention policy before reuse.

This only works cleanly when ownership is clear. If an EOR uses a local-partner shell, who actually owns the laptop becomes a murky negotiation. Because we own our Indian entity, we are the direct legal owner, so recovery is an instruction, not a plea through a middle layer.

Recovery tied to Full and Final almost always works, while goodwill alone often does not. See how this fits our wider model on our retention-first EOR page, or talk it through on a consultation.

Ready to hire in India?

Drop your work email · we'll set up a 20-min intro call within 24 hours. Tell us what you're building; we'll tell you whether we're the right fit.

We reply in business hours (IST). Never spam, never share your email.