Table of contents (37)

- Payroll Compliance Basics

- The first-hire trap nobody warns you about

- Compliance is the floor, not the ceiling

- PF and ESI Rates

- The numbers, with their primary sources

- The mid-period ESI rule that catches everyone

- New Labour Code 2025-26

- What the 50% rule actually does

- Fix it at the offer, not the payslip

- PT, Gratuity, and Bonus

- Professional tax: one country, many rulebooks

- Gratuity, LWF, and bonus

- India Filing Calendar

- The master compliance calendar

- Why the calendar breaks: the swarming problem

- Penalties and Misclassification

- The penalty mechanics

- The misclassification trap

- Audit-ready is the only ready

- Paying India From Abroad

- How the money actually moves

- PE risk: the tax bill nobody mentions

- PEO vs EOR Options

- The PEO myth

- Your three real paths

- Where the tipping point really sits

- India-Native vs Generalists

- The structural difference most founders miss

- What the reviews actually say

- Versatile vs Wisemonk

- Versatile versus Wisemonk, side by side

- Compliance is the floor, not the ceiling

- DPDP Act and Payroll

- What DPDP actually means for payroll

- Five-Day Go-Live

- The 5-day go-live sequence

- Three things to do before payroll

Payroll Compliance in India: PF, ESI, TDS, Gratuity, PT, and the Filing Calendar That Trips Most Employers

Discover how payroll compliance in India works: PF, ESI, TDS, gratuity, PT, and the filing calendar that trips most foreign employers.

Q1: What is payroll compliance in India, and why does it trip up foreign employers?

Payroll compliance in India means correctly deducting, depositing, and filing the recurring statutory obligations, including Provident Fund (PF), Employees' State Insurance (ESI), TDS on salary, professional tax (PT), gratuity, and labour welfare fund, under each applicable Act and state rule, on a fixed monthly, quarterly, and annual calendar. It trips foreign employers because deadlines are unforgiving, rules vary by state, and one missed filing can trigger a statutory audit and back-pay exposure.

The first-hire trap nobody warns you about

Hiring your first engineer in India looks simple until you try to do it from the US. You send an offer, wire some money, and assume payroll is a spreadsheet problem. It is not.

The moment that offer is accepted, you are now a legal employer under Indian law. That status carries deductions, deposits, and filings that started running the day your hire joined.

Most founders I work with discover this at the worst time. Either fundraising diligence asks for clean India payroll records, or the team scales past ten people and manual tracking falls apart. For teams at that stage, an Employer of Record in India absorbs these obligations from day one.

What "compliance" actually means in practice

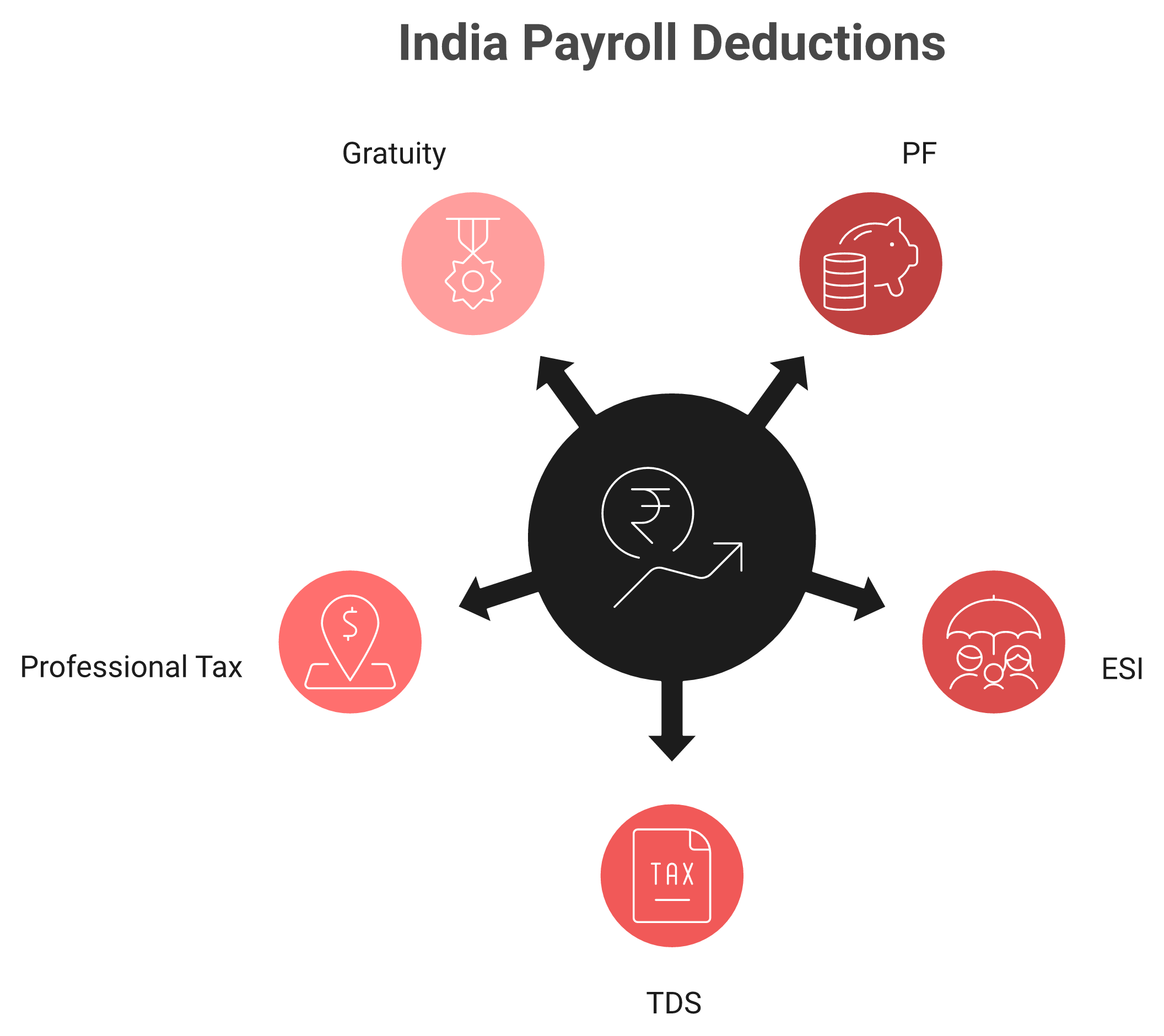

One offer letter quietly becomes several simultaneous obligations. Here is what fires at once for a single salaried hire:

PF (Provident Fund): retirement contribution filed with the EPFO each month.

ESI (Employees' State Insurance): medical and cash benefit cover, filed with the ESIC.

TDS on salary: income tax deducted at source, deposited by the 7th.

Professional tax: a state levy with its own slabs and dates.

Gratuity: a long-service payout that starts accruing from month one.

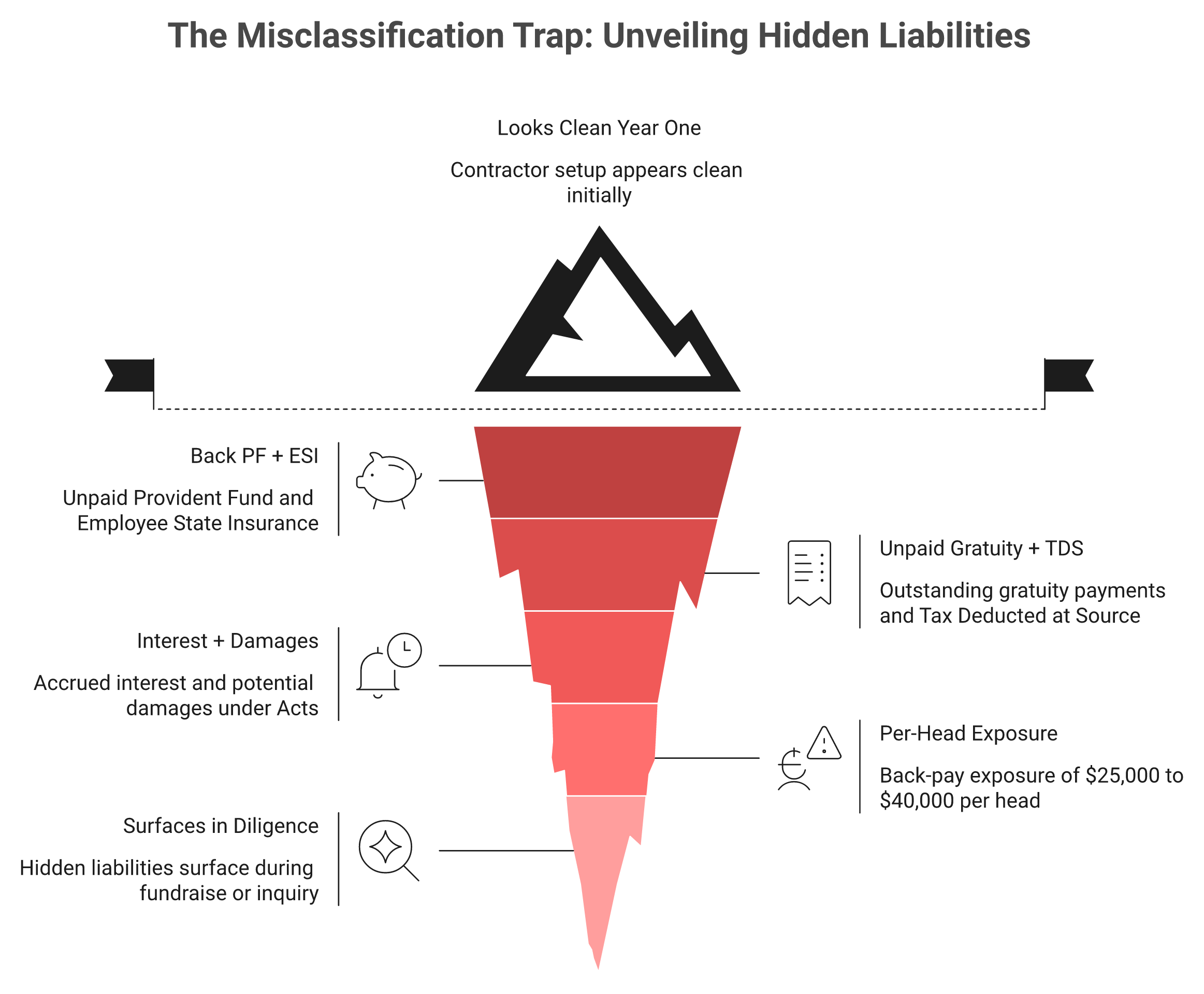

Treat a full-time engineer as an "independent contractor" to skip this, and you invite the bill nobody budgets for. Misclassification can create roughly $25,000 to $40,000 in back-pay exposure per head, and it usually surfaces months later during diligence. You can gauge your own exposure with this misclassification risk quiz.

Compliance is the floor, not the ceiling

Here is the read the category gets backwards. Founders treat compliance as the finish line, when it is really the entry fee.

Clean statutory records protect three things you care about: a smooth fundraise, a painless audit, and a future transition to your own entity without flags. After six years running Versatile's India C2H and EOR operations across Bengaluru, Hyderabad, and Pune, I can tell you the failure is almost never intent. The rules simply do not wait for you to learn them. This is why founders increasingly choose to hire in India without an entity.

I might be slightly contrarian here, but the "good hire who stays" matters more than the "legal hire on paper." Compliance keeps you safe. It does not keep your team.

Q2: Which statutory deductions apply, and what are the exact PF and ESI rates?

Three deductions hit every payslip. PF is 12% employee plus 12% employer on Basic+DA up to a Rs 15,000 ceiling, with 8.33% of the employer share diverted to pension (EPS), roughly Rs 1,800 each side at the cap. ESI is 0.75% employee plus 3.25% employer for wages up to Rs 21,000 (Rs 25,000 for persons with disabilities). TDS on salary is deducted monthly under Section 192 per the employee's slab.

The numbers, with their primary sources

These are not estimates. Each rate below maps to a government notification or official rate table, not a blog summary. Our India payroll compliance calculation applies each of these automatically.

India Statutory Deduction Rates | ||||

Deduction | Who pays | Rate | Ceiling / limit | Primary source |

|---|---|---|---|---|

PF | Employee + employer | 12% + 12% on Basic+DA | Rs 15,000 wage ceiling (~Rs 1,800 each) | EPFO Present Rates of Contribution |

EPS (within employer PF) | Employer share | 8.33% diverted | Capped to Rs 15,000 wage | EPFO |

ESI | Employee + employer | 0.75% + 3.25% | Rs 21,000 wage limit (Rs 25,000 PwD) | ESIC Contribution (w.e.f. 01.07.2019) |

TDS on salary | Employer deducts | Per income slab | No flat rate; slab-based | Income-tax Act 1961, Section 192 |

A note on the Rs 176 figure: ESI exempts employees earning an average daily wage up to Rs 176 from the employee share, while the employer still contributes.

The mid-period ESI rule that catches everyone

Here is the rule that surprises even seasoned HR teams. If an employee's wage crosses Rs 21,000 in the middle of a contribution period, you do not stop ESI.

You keep deducting and depositing on actual wages until that six-month cycle closes. The contribution periods run April to September and October to March. Coverage only ends at the start of the next cycle.

From what surfaces when you actually run this, the stop-immediately instinct is the single most common ESI error I see in inherited payrolls. On Versatile India payroll, all three deductions run under our own PF registration and ESIC code, not a downstream partner shell, so the rates above are what we actually remit.

Q3: How does the New Labour Code 2025-26 and the 50% wage rule change your payroll?

Under the Code on Wages, effective 21 November 2025, "wages" (Basic + DA + retaining allowance) must be at least 50% of total remuneration. Where allowances exceed half of CTC, the excess is added back to wages, which raises the PF and gratuity base. Because statutory PF stays capped at the Rs 15,000 ceiling, most employees' take-home does not change. Legacy salary stacks built to minimise Basic are the ones that break.

What the 50% rule actually does

The old Indian salary trick was simple. Keep Basic low, pile on allowances, and shrink the PF and gratuity base. The new codes close that gap.

Now the law sets a floor. Your wage components must be at least half of total pay, and anything you stuffed into "special allowance" above that line gets pulled back into wages for statutory math.

A worked example

Take a Rs 10,00,000 annual CTC built the old way, with Basic at just 30%.

Old structure: Basic Rs 3,00,000 (30%), allowances Rs 7,00,000 (70%).

New rule: wages must reach Rs 5,00,000 (50%), so Rs 2,00,000 of allowance is added back.

PF effect: the statutory base stays capped at Rs 15,000 a month, so PF holds near Rs 1,800 each side.

Take-home effect: usually flat, because PF is capped, not uncapped.

So the scare headline ("your costs explode") is mostly wrong for PF. The real exposure is gratuity, which accrues on the higher wage base. You can model the true loaded figure with our employee cost calculator.

Fix it at the offer, not the payslip

This is the part legacy payroll systems quietly get wrong. Many never restructured templates after the codes landed, so they file on a non-compliant base.

We rebuilt every Versatile offer template the week the codes took effect. A restructure done after the first payslip is a correction, and corrections are exactly what diligence flags. Your Monday action is plain: audit every open offer letter and confirm Basic+DA is at least 50% of CTC before anyone signs. If you would rather hand this off entirely, our managed payroll service rebuilds the salary stack for you.

Q4: Beyond PF and ESI, how do professional tax, gratuity, LWF, and bonus actually work?

These are the obligations that vary most. Professional tax is state-administered: Maharashtra needs dual PTRC+PTEC registration with monthly filing, Karnataka files monthly, and Tamil Nadu files biannually. Gratuity is payable after five years of continuous service (4 years plus 240 days qualifies in the fifth year), computed as 15/26 × last-drawn Basic+DA × completed years, capped at Rs 20 lakh tax-exempt, and accrues from month one at 4.81% of Basic+DA. Labour welfare fund and statutory bonus apply on top.

Professional tax: one country, many rulebooks

There is no single national PT rule. Each state sets its own registration type, cycle, and slab, so a multi-state team means multiple PT calendars running at once. Our India payroll outsourcing team holds these registrations where clients hire.

Professional Tax by State | ||

State | Registration | Filing cycle |

|---|---|---|

Maharashtra | Dual: PTRC (employees) + PTEC (entity) | Monthly slab + annual return |

Karnataka | Single PT enrolment | Monthly |

Tamil Nadu | PT enrolment | Biannual (June, December) |

Delhi | No professional tax | Strict Shops & Establishments rules instead |

We understand the difference between Maharashtra's dual PTRC/PTEC setup, Karnataka's monthly cycle, and Tamil Nadu's biannual filing because we hold those registrations where our clients hire. So a Pune hire and a Chennai hire run on their correct, separate cycles.

Gratuity, LWF, and bonus

Gratuity feels far away to a Western founder, but it starts on day one. You accrue it monthly at 4.81% of Basic+DA, even though it only vests later. You can estimate the payout with our gratuity calculator.

Eligibility and the 240-day rule

An employee is eligible after five years of continuous service. Courts have settled that 4 years plus 240 days in the fifth year counts as five years. The formula is 15/26 × last-drawn Basic+DA × completed years, tax-exempt up to Rs 20 lakh.

Then two more items sit on top. Labour welfare fund is a small state contribution, usually paid twice a year, and statutory bonus runs under the Payment of Bonus Act 1965; customary bonus operates in a separate field and does not clash with it.

The standard read treats these as archaic. To Indian employees, PF and gratuity are emotionally and legally non-negotiable, and Versatile provisions gratuity from day one so the books never carry a surprise. When you eventually outgrow this model, our EOR vs entity in India guide maps the transition.

Q5: What does the actual filing calendar look like, and which deadlines trip most employers?

The recurring calendar is tight. TDS is deposited by the 7th of each month, PF (ECR) and ESI contributions by the 15th, and Form 24Q quarterly returns by 31 July, 31 October, 31 January, and 31 May. Form 16 goes to each employee by 15 June, and annual returns like the POSH report fall due by 31 January. Most employers miss these not from neglect, but from running them all at once across multiple states.

The master compliance calendar

Here is the cadence that runs for every salaried hire in India. Print it, pin it, or hand it to whoever owns payroll. Our India payroll compliance calculation tracks each of these dates automatically.

India Statutory Filing Calendar | ||

When | What is due | Filed with |

|---|---|---|

7th monthly | TDS on salary deposited | Income Tax / TRACES |

15th monthly | PF ECR (Electronic Challan cum Return) | EPFO |

15th monthly | ESI contribution | ESIC |

31 Jul, 31 Oct, 31 Jan, 31 May | Form 24Q quarterly TDS return | TRACES |

15 June | Form 16 to each employee | Employer to employee |

31 January | POSH annual report | District Officer |

ECR means the monthly PF challan-cum-return; Form 24Q is the quarterly salary TDS filing.

Why the calendar breaks: the swarming problem

Here is the part the standard read gets backwards. Western founders expect compliance to run in a line, one task closed before the next opens.

India does not work that way. In Indore there is no queue at a counter; people swarm it, and many things move at once. Indian compliance filing is the same, with several deadlines firing in parallel.

The three deadlines I see slip most

From what surfaces when you actually run multi-state payroll, the same three trip people up:

PF ECR confusion: unexempted establishments file by the 15th, exempted trusts by the 25th. Mixing the two invites damages.

Mid-period ESI: an employee crossing Rs 21,000 mid-cycle still needs contributions until the period closes.

Q4 Form 24Q Annexure II: the year-end annexure feeds Form 16, so a Q4 slip delays every employee's tax statement.

I could be slightly off on edge cases, but I have not seen a manual tracker survive past ten hires. At Versatile, every date above sits inside our own managed payroll workflow, so the founder gets a payslip, not a deadline tracker.

Q6: What happens when you get it wrong, including penalties, audits, and the misclassification trap?

Getting it wrong is expensive and delayed. Late PF and ESI attract interest and damages, late TDS triggers interest plus a Section 234E fee, and treating a full-time engineer as an "independent contractor" can create $25,000 to $40,000 in back-pay exposure per head. The cruelty is timing. Misclassification often surfaces months later during fundraising diligence, exactly when clean records matter most.

The penalty mechanics

Each statute has its own teeth. None of them are forgiving, and interest compounds quietly.

TDS: late deposit draws interest, and late filing of Form 24Q adds a Rs 200-per-day fee under Section 234E.

PF: late deposit attracts interest plus damages under the EPF and MP Act, 1952.

ESI: delayed contributions carry interest at 12% per annum and further damages.

The misclassification trap

This is the one that ambushes US founders. You hire an engineer "as a contractor" to dodge PF and ESI, and it feels clean for a year. You can check your own exposure with our misclassification quiz.

Then diligence, a resignation, or an EPFO inquiry reclassifies them as an employee. Now you owe back PF, ESI, gratuity, and TDS, often Rs 20 lakh-plus per head. Slow contracts and mystery FX charges hide the same way; the surprise shows up months later.

"We had to constantly remind them of the fees agreed so that we weren't over charged. Everything was VERY time consuming. It took three months to onboard our first 3 individuals."

Verified User in Information Technology and Services Deel G2 Verified Review

"The PF transfer for employees after terminating their employment with Velocity was very poor. There was limited help, delayed responses."

Verified User in Computer Software Velocity Global G2 Verified Review

Audit-ready is the only ready

CFOs at Series A to C startups do not ask for "good" payroll. They ask for clean, so a future move to a captive center never trips a diligence flag. This is the core case for an Employer of Record in India.

I might be blunt here, but audit-ready is not a feature you bolt on later. When our clients graduate from Versatile EOR to their own entity, the books hand over clean, because every filing was already under our registrations. Our EOR vs entity in India guide maps that handover.

Q7: How do you actually pay an India team from abroad, including USD invoicing, FEMA, and PE risk?

Paying an India team from abroad runs through India's foreign-exchange rules. Routing salaries through a foreign holding company and converting from INR often adds a 3% to 5% FX markup, while inbound capital into an Indian entity triggers FEMA reporting such as the FC-GPR filing. Running employees without an entity also raises permanent-establishment (PE) risk, where a foreign company is deemed taxable in India. Invoicing in USD directly from an Indian entity avoids both problems.

How the money actually moves

Most global platforms move your dollars through a foreign holding company, convert to rupees, and pay the employee. Each hop adds a cut. Our guide on how to pay employees in India walks through the cleaner route.

That conversion is where the quiet 3% to 5% FX markup lives, and it rarely shows on the invoice. FC-GPR (Foreign Currency-Gross Provisional Return) is the RBI filing required when foreign money buys shares in an Indian entity, governed by FEMA, 1999.

"I find Deel to be absurdly expensive. They charge a high amount of fees for transferring money to my bank account."

Juan Camilo O. Deel G2 Verified Review

PE risk: the tax bill nobody mentions

Permanent establishment means India decides your foreign company has a taxable presence here. Run employees directly without an entity, and you can trigger it. You can gauge this with our permanent establishment risk quiz.

The consequence is corporate tax on India-attributable profit, plus penalties. The standard "just pay them as contractors" advice quietly walks founders straight into this.

The clean structure

Invoicing in USD straight from a registered Indian entity removes both the FX leakage and the PE ambiguity.

"Invoicing in USD meant zero exchange rate surprises. The compliance rigour is genuinely impressive, every statutory filing reviewed before submission."

Vedant T., Founder Versatile G2 Verified Review

At Versatile, we invoice you in USD from our own Indian entity, with no foreign holding company and no INR conversion on your side. Your month-end close stays predictable, and the PE question never opens.

Q8: Why doesn't a US-style PEO work in India, and what are your real options?

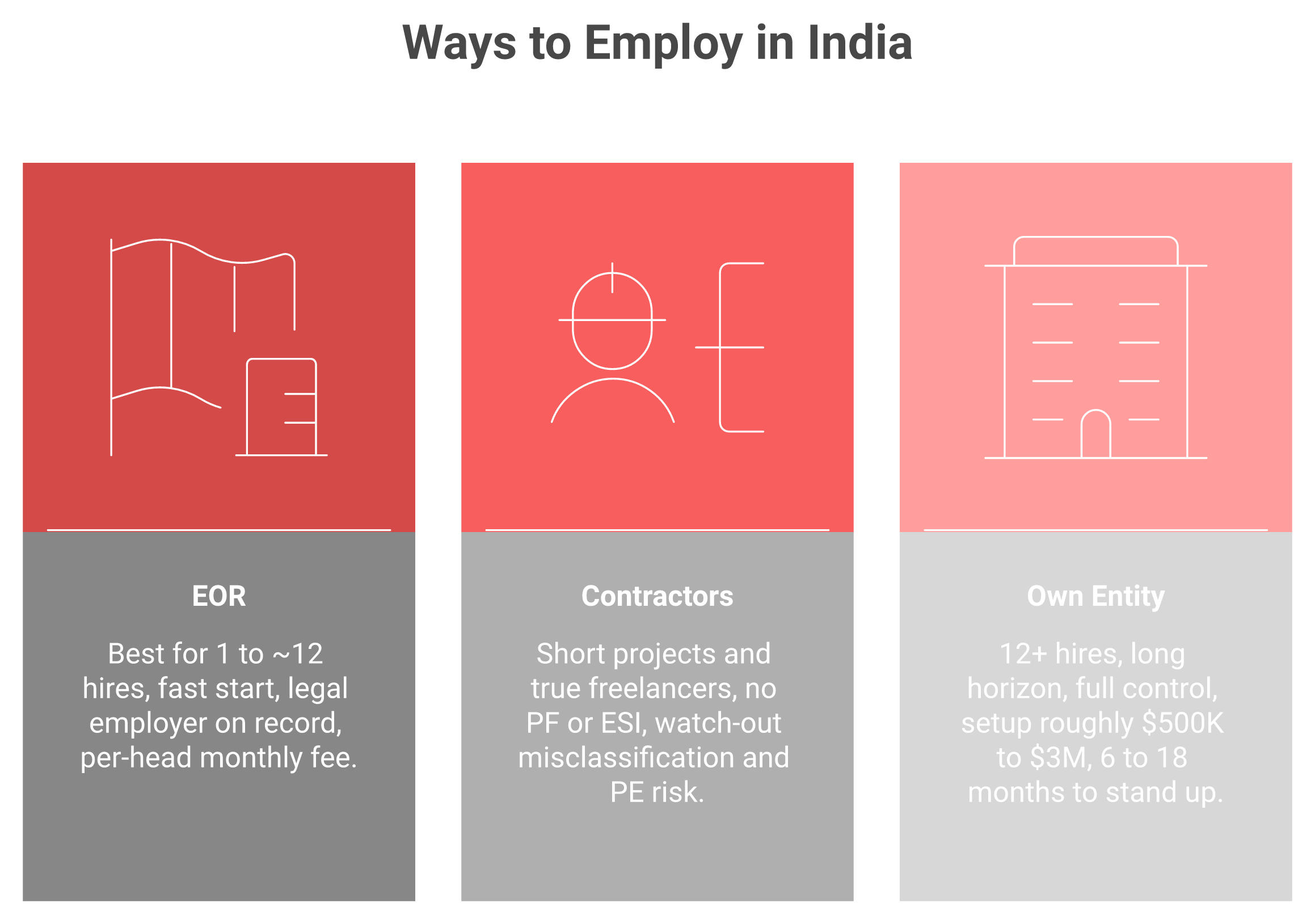

A US-style co-employment PEO does not legally exist under Indian labour law. So founders without an Indian entity have three real options: hire through an Employer of Record (EOR) that becomes the legal employer, engage independent contractors (with misclassification risk), or set up their own entity. The entity tipping point usually arrives around 10 to 12 hires, where setup and ongoing compliance cost begins to outweigh EOR fees.

The PEO myth

In the US, a PEO co-employs your staff and shares liability. Founders assume the same model ports to India. Our PEO India page explains where the analogy breaks.

It does not. Indian labour law has no co-employment construct, so the only way to employ without your own entity is through an EOR that is the full legal employer on record.

Your three real paths

Here is the honest decision frame. Each fits a different stage and cash position. You can model the crossover with our EOR vs entity calculator.

India Employment Options Compared | ||

Option | Best for | Watch-out |

|---|---|---|

EOR | 1 to ~12 India hires, fast start | Per-head monthly fee |

Contractors | Short projects, true freelancers | Misclassification, PE risk |

Own entity | 12+ hires, long horizon | ~$500K to $3M and 6 to 18 months for a full captive |

"We looked at setting up a subsidiary and quickly realized it would take 6 months, cost tens of thousands in legal and registration fees, and require ongoing compliance work we had no expertise in."

Verified User in Information Technology and Services Versatile G2 Verified Review

Where the tipping point really sits

From the placements we have converted to full-time over six years, the entity decision rarely makes sense before roughly twelve hires. Below that, the math and the compliance load favor an EOR. If you would rather skip the entity entirely, see how to hire in India without an entity.

"It let us hire in India without standing up an entity, which would've been overkill for our size."

Angad S., Founder at Moonshot Versatile G2 Verified Review

I could be wrong for a capital-heavy team racing to 50 hires. But for most US founders making their first India hires, Versatile is built for that pre-tipping-point window, and we hand over a clean entity transition later with no exit fee.

Q9: How do India-native EORs compare with global generalists like Deel, Remote, and G-P?

Global EOR platforms cover 90 to 150 countries and run India through local partner entities, which spreads their India compliance depth thin and often adds a 3% to 5% FX markup and 10 to 14-day onboarding. India-native EORs own their Indian entity, file PF, ESI, TDS, and professional tax under their own registrations, and can invoice in USD directly. For a small India team, depth and structure usually matter more than country count.

The structural difference most founders miss

Generalists are built wide, not deep. India is one flag of 150 on their map, and behind that flag sits a local partner entity, not their own. Our Deel alternatives in India page breaks down the gap.

Think of it like AWS regions. Breadth is real, but depth in any single region is a separate engineering problem. India is that region for payroll, and shallow coverage shows up as missed labour-code nuance.

India-Native EOR vs Global Generalist | ||

Factor | Global generalist | India-native EOR |

|---|---|---|

Countries | 90 to 150 | India only |

India entity | Local partner shell | Owned entity |

FX | 3% to 5% markup reported | USD direct, no markup |

Onboarding | 7 to 14 days | As fast as 5 days |

India compliance depth | Thin at state level | Multi-state PT, labour code |

What the reviews actually say

The pattern in generalist reviews is consistent: convenient interface, painful support, and slow India-specific work. You can see the head-to-head on our Versatile vs Deel comparison.

"The majority of their support team is helpful, but are often constrained by internal limitations. Everything was VERY time consuming. It took three months to onboard our first 3 individuals."

Verified User in Information Technology and Services Deel G2 Verified Review

"I encountered many frustrations with the onboarding, and continue to find the portal difficult to use. My contract had the wrong start date and other errors."

Verified User in Non-Profit Organization Management Velocity Global G2 Verified Review

When each one actually fits

I want to be fair here, because the answer is genuinely "it depends."

Pick a generalist when you hire across five-plus countries and need one dashboard.

Pick an India Employer of Record when India is your real team and diligence cares about clean records.

At Versatile, we invoice you in USD straight from our own Indian entity, with no foreign holding company and no INR conversion. If you need fifteen countries, we are honestly the wrong call, and I will say so on the first call.

Q10: How is Versatile different from Wisemonk and other India-native EORs?

Among India-native EORs, the differences are operational. Versatile leads with a 5-day contractual onboarding SLA, no setup or exit fees, first month free, an owned Indian entity, and a people-first model: culture-fit hiring on 50 behavioral parameters, a 90-day Success Coach, and a 6-month replacement guarantee. Wisemonk is also India-native, with strong G2 standing, but its per-tier pricing for different salary bands is not fully transparent and usually needs a sales conversation. The distinction is the "good hire who stays" versus the "legal hire on paper."

Versatile versus Wisemonk, side by side

Wisemonk is a credible India-native operator, and I respect the build. Here is the honest contrast, expanded on our Wisemonk vs Versatile Club page.

Versatile vs Wisemonk | ||

Factor | Versatile | Wisemonk |

|---|---|---|

India entity | Owned | India-native |

Onboarding | 5-day contractual SLA | 24 to 72 hours stated |

Pricing clarity | Published, no setup/exit fee, first month free | Tiered, often needs a sales call |

Retention model | 50 behavioral parameters, 90-day Success Coach, 6-month replacement | No published replacement guarantee |

Support | Founder on WhatsApp | Support team |

Wisemonk reviewers like the structure, and they also flag response lag from a small team.

"I've noticed that their support query responses can occasionally take a bit longer sometimes, likely due to a relatively small team."

Verified User in Financial Services Wisemonk G2 Verified Review

Compliance is the floor, not the ceiling

Here is where the category gets it backwards. Every EOR can file PF and ESI; that is table stakes, not a moat. See our take on Wisemonk alternatives.

The harder problem is the hire who stays. Nearly 30% of India IT resumes carry discrepancies, so culture-fit screening, a 90-day Success Coach, and a 6-month replacement guarantee solve a problem pure compliance never touches. This is the heart of our retention-first EOR in India model.

"Founder is just a call away. Extremely helpful in resolving all our queries. The process is super smooth to setup India EOR."

surbhi m. Versatile G2 Verified Review

You reach me on WhatsApp, not a ticket queue. I might be biased, but the person who built Versatile answering your payroll question at 11pm your time is the feature I would not trade.

Q11: Does the DPDP Act change how you handle payroll and employee data?

Yes. The Digital Personal Data Protection (DPDP) Act, 2023, with Rules notified on 14 November 2025, is India's first comprehensive data-privacy law, and payroll and HR data fall squarely within it. Processing employee data for employment is allowed as a "legitimate use," but breach-notification, security safeguards, and individual-rights handling all apply, with most employer obligations enforceable by mid-2027. 2026 is the year to map where payroll data lives.

What DPDP actually means for payroll

Your payroll holds PAN, bank details, salary, and address. That is personal data, and DPDP now governs how you collect, store, and protect it. Our managed payroll service processes all of this under our own entity.

The good news: you do not need separate consent to run payroll. Employment processing is a "legitimate use," which means using data for the job itself. The catch is the duties that come with it, namely security safeguards and reporting a breach.

Your Monday actions before 2027

The enforcement runway is staggered, so 2026 is a build year, not a panic year.

Map your payroll data: list where PAN, salary, and bank details sit.

Stand up a breach process: know who reports, and how fast.

Vet your vendors: ask your EOR or payroll tool how they handle DPDP.

I could be cautious to a fault here, but diligence is already starting to ask about data handling, not just statutory filings. At Versatile, we process payroll data under our own entity and DPDP obligations, so that is one more thing a lean founder does not have to architect alone. Our broader EOR services in India fold this in by default.

Q12: How do you go live in five days, and what should you do this Monday?

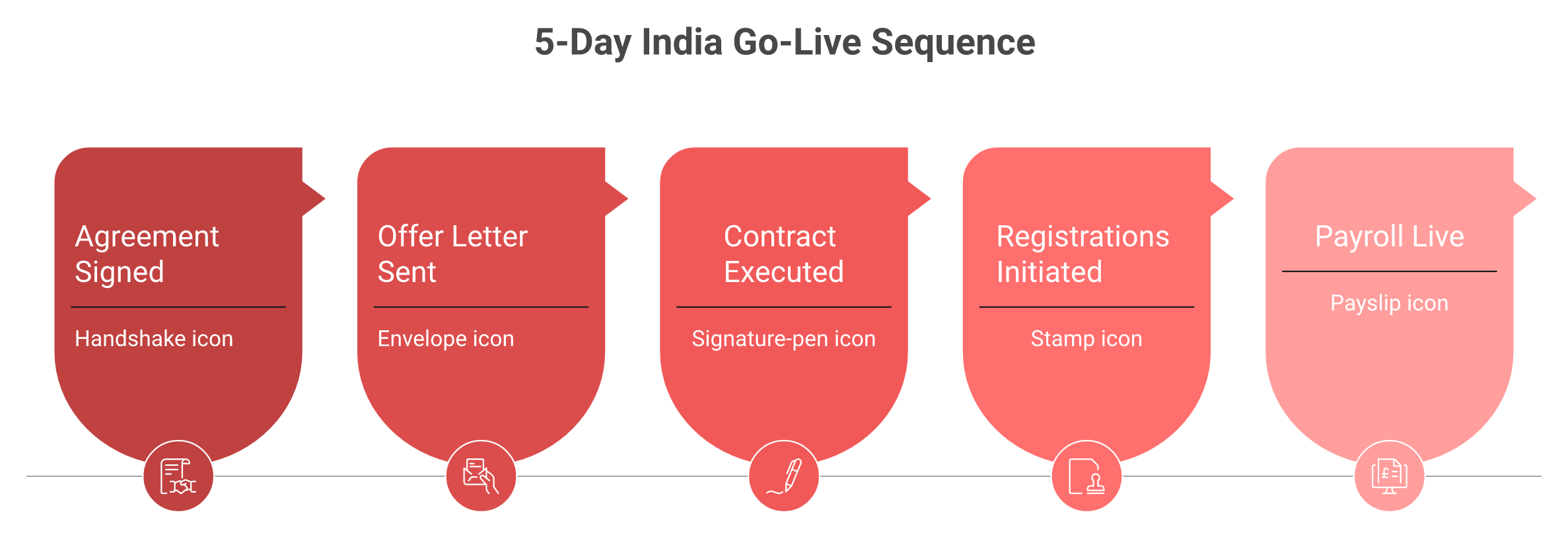

Going live with an India hire can take five working days, not five weeks: Day 1 agreement signed, Day 2 offer letter sent, Day 3 contract executed, Day 4 statutory registrations (PF, ESI, professional tax) initiated, and Day 5 payroll live. This Monday, confirm Basic+DA is at least 50% of CTC, classify the role correctly as an employee rather than a contractor, and decide your model, namely EOR now and entity later.

The 5-day go-live sequence

Speed is not a marketing line; it is a sequence you can hold a vendor to. Here is the cadence we run when you hire employees in India through us.

Day 1: agreement signed.

Day 2: offer letter sent to the hire.

Day 3: contract executed.

Day 4: PF, ESI, and professional tax registrations initiated.

Day 5: payroll live.

"It replied to our form in about four hours with a draft offer letter already attached. The hire was onboarded in four days. USD invoice landed clean, no FX markup, no setup fee, no surprises."

Verified User in Information Technology and Services Versatile G2 Verified Review

Three things to do before payroll

You can act on these today, regardless of who you hire through. To pressure-test the cost side, run our cost of hiring in India breakdown.

Fix the salary stack: Basic+DA at least 50% of CTC, so the labour codes do not bite later.

Classify correctly: a full-time engineer is an employee, not a contractor.

Pick your model: EOR while you are under roughly twelve hires, entity after.

One small cross-cultural habit

A bonus from six years of running offshore teams. After any call, recap the key points in a short email.

Indian teammates often will not say "I did not understand"; deference fills the gap with silence. So ask open questions like "where are we on the schedule," never closed "are we on track" ones.

Where my head is right now is this: in the next two years, India stops being one flag on a global EOR map and becomes its own specialist category, where owned-entity operators quietly take the generalists' India revenue. If you are making that first India hire, tell me what you are building. You will reach me, Sagar, directly on WhatsApp, not a ticket queue. When you are ready, book a consultation with us.

FAQs

What does payroll compliance in India actually include?

Payroll compliance in India means correctly deducting, depositing, and filing every recurring statutory obligation under the right Act and state rule, on time, every cycle. It is not one task; several fire at once the moment a hire joins.

- Provident Fund (PF): a retirement contribution filed monthly with the EPFO.

- Employees' State Insurance (ESI): medical and cash-benefit cover filed with the ESIC.

- TDS on salary: income tax deducted at source and deposited by the 7th.

- Professional tax: a state levy with its own slabs and dates.

- Gratuity: a long-service payout that starts accruing from month one.

On top of these sit labour welfare fund, statutory bonus, and annual filings like Form 16 and the POSH report. The hard part is not any single rule; it is running them in parallel across multiple states, each with a different cycle. We built our managed payroll service exactly for this, so a founder gets a payslip rather than a deadline tracker. Miss a filing and you can trigger interest, damages, and a statutory audit, which is why we treat clean records as the entry fee, not the finish line.

What are the exact PF and ESI contribution rates in India?

Three deductions hit every Indian payslip, and the rates are set by government rate tables, not convention.

- PF: 12% employee plus 12% employer on Basic+DA, up to a Rs 15,000 wage ceiling, which is roughly Rs 1,800 each side at the cap. Within the employer share, 8.33% is diverted to the pension scheme (EPS).

- ESI: 0.75% employee plus 3.25% employer for wages up to Rs 21,000 (Rs 25,000 for persons with disabilities).

- TDS on salary: deducted monthly under Section 192 per the employee's income slab, with no flat rate.

One rule trips even seasoned teams: if an employee's wage crosses Rs 21,000 mid-period, you do not stop ESI immediately. You keep contributing on actual wages until the six-month contribution cycle closes. On our India payroll service, all three deductions run under our own PF registration and ESIC code, not a downstream partner shell, so the rates we quote are the rates we actually remit. You can also model the fully loaded cost of any salary with our employee cost calculator before you extend an offer.

How does the New Labour Code 2025-26 and the 50% wage rule change payroll?

Under the Code on Wages, effective 21 November 2025, "wages" (Basic plus DA plus retaining allowance) must be at least 50% of total remuneration. Where allowances exceed half of CTC, the excess is added back into wages for statutory math, which raises the PF and gratuity base.

Here is the part the scare headlines get wrong. Because statutory PF stays capped at the Rs 15,000 wage ceiling, most employees' take-home does not change much. The real exposure is gratuity, which accrues on the higher wage base at 4.81% of Basic+DA.

- Old trick: keep Basic low, pile on allowances, shrink the PF and gratuity base.

- New floor: wage components must reach at least 50% of total pay.

- Your fix: restructure at the offer stage, not after the first payslip.

Corrections made after payroll has run are exactly what diligence flags. We rebuilt every offer template the week the codes took effect, and our India payroll compliance calculation applies the 50% rule automatically. Your Monday action is simple: audit every open offer letter and confirm Basic+DA is at least 50% of CTC before anyone signs.

What are the penalties for getting India payroll compliance wrong?

Getting it wrong is expensive, and the bill is usually delayed, which is what makes it dangerous. Each statute carries its own teeth, and interest compounds quietly while you assume everything is fine.

- TDS: late deposit draws interest, and late filing of Form 24Q adds a Rs 200-per-day fee under Section 234E.

- PF: late deposit attracts interest plus damages under the EPF and MP Act, 1952.

- ESI: delayed contributions carry interest at 12% per annum, plus further damages.

The costliest mistake is misclassification. Treating a full-time engineer as an "independent contractor" to skip PF and ESI can create roughly $25,000 to $40,000 in back-pay exposure per head, often surfacing during a fundraise, a resignation, or an EPFO inquiry, exactly when clean records matter most. You can pressure-test your own setup with our misclassification quiz. When our clients later move from EOR to their own entity, the books hand over clean because every filing already sat under our registrations, which is the case for choosing an India Employer of Record from day one.

How do you pay an India team from abroad without FX losses or PE risk?

Paying an India team from abroad runs through India's foreign-exchange rules, and the default route quietly leaks money. Most global platforms move your dollars through a foreign holding company, convert to rupees, and pay the employee, with each hop adding a cut.

- FX markup: that conversion is where a quiet 3% to 5% markup lives, and it rarely shows on the invoice.

- FEMA reporting: inbound capital into an Indian entity triggers filings such as FC-GPR under FEMA, 1999.

- Permanent establishment (PE) risk: running employees directly without an entity can make your foreign company taxable in India.

The clean structure is to invoice in USD straight from a registered Indian entity, which removes both the FX leakage and the PE ambiguity. That is exactly how our pay employees in India model works: we invoice you in USD from our own Indian entity, with no foreign holding company and no INR conversion on your side. Your month-end close stays predictable, and the PE question never opens. If you want to gauge your exposure first, try our permanent establishment risk quiz.

Is an EOR cheaper than setting up your own entity in India?

For most foreign companies making their first India hires, yes, an Employer of Record is both cheaper and faster than standing up an entity. A US-style co-employment PEO does not legally exist under Indian labour law, so your real options narrow to three.

- EOR: best for one to roughly twelve hires, fast start, per-head monthly fee.

- Contractors: fine for short projects and genuine freelancers, but they carry misclassification and PE risk.

- Own entity: sensible past twelve hires on a long horizon, but a full captive can cost hundreds of thousands of dollars and take 6 to 18 months.

The tipping point usually arrives around 10 to 12 hires, where entity setup and ongoing compliance cost begin to outweigh EOR fees. Below that, the math and the compliance load favor an EOR. You can model your own crossover with our EOR vs entity calculator, and our deeper EOR vs entity in India guide maps the transition. We are built for that pre-tipping-point window, and we hand over a clean entity later with no exit fee.

Does the DPDP Act change how you handle payroll and employee data?

Yes. The Digital Personal Data Protection (DPDP) Act, 2023, with Rules notified on 14 November 2025, is India's first comprehensive data-privacy law, and payroll and HR data fall squarely within it. Your payroll holds PAN, bank details, salary, and address, all of which count as personal data.

The good news is that you do not need separate consent to run payroll, because employment processing qualifies as a "legitimate use." The catch is the duties that come with it: security safeguards, breach notification, and individual-rights handling, with most employer obligations enforceable by mid-2027.

- Map your data: list where PAN, salary, and bank details sit.

- Stand up a breach process: know who reports, and how fast.

- Vet your vendors: ask your EOR or payroll tool how they handle DPDP.

Diligence is already starting to ask about data handling, not just statutory filings, so 2026 is a build year rather than a panic year. We process payroll data under our own entity and DPDP obligations as part of our EOR services in India, which is one more thing a lean founder does not have to architect alone.

How fast can you go live with an India hire?

Going live with an India hire can take five working days, not five weeks, if the sequence is run tightly. Speed is not a marketing line; it is a process you can hold any vendor to.

- Day 1: agreement signed.

- Day 2: offer letter sent to the hire.

- Day 3: contract executed.

- Day 4: PF, ESI, and professional tax registrations initiated.

- Day 5: payroll live.

Before you start, three things are worth confirming this Monday: that Basic+DA is at least 50% of CTC, that the role is classified correctly as an employee rather than a contractor, and that you have picked your model, namely EOR now and entity later. We run this exact five-day cadence when you hire employees in India through us, and you reach the founder directly on WhatsApp rather than a ticket queue. When you are ready to map your first hire, you can book a consultation with us and we will walk the sequence with you.

Ready to hire in India?

Drop your work email · we'll set up a 20-min intro call within 24 hours. Tell us what you're building; we'll tell you whether we're the right fit.

We reply in business hours (IST). Never spam, never share your email.